Let’s be honest: most budgeting advice is written by people who have never impulsively DoorDashed $42 worth of Chick-fil-A because dinner “emotionally wasn’t happening tonight,” never panic-bought something on Amazon at 10:47 PM, and definitely never had kids scream “I NEED THIS!” at Target.

And then there’s the advice from financial celebrities yelling,

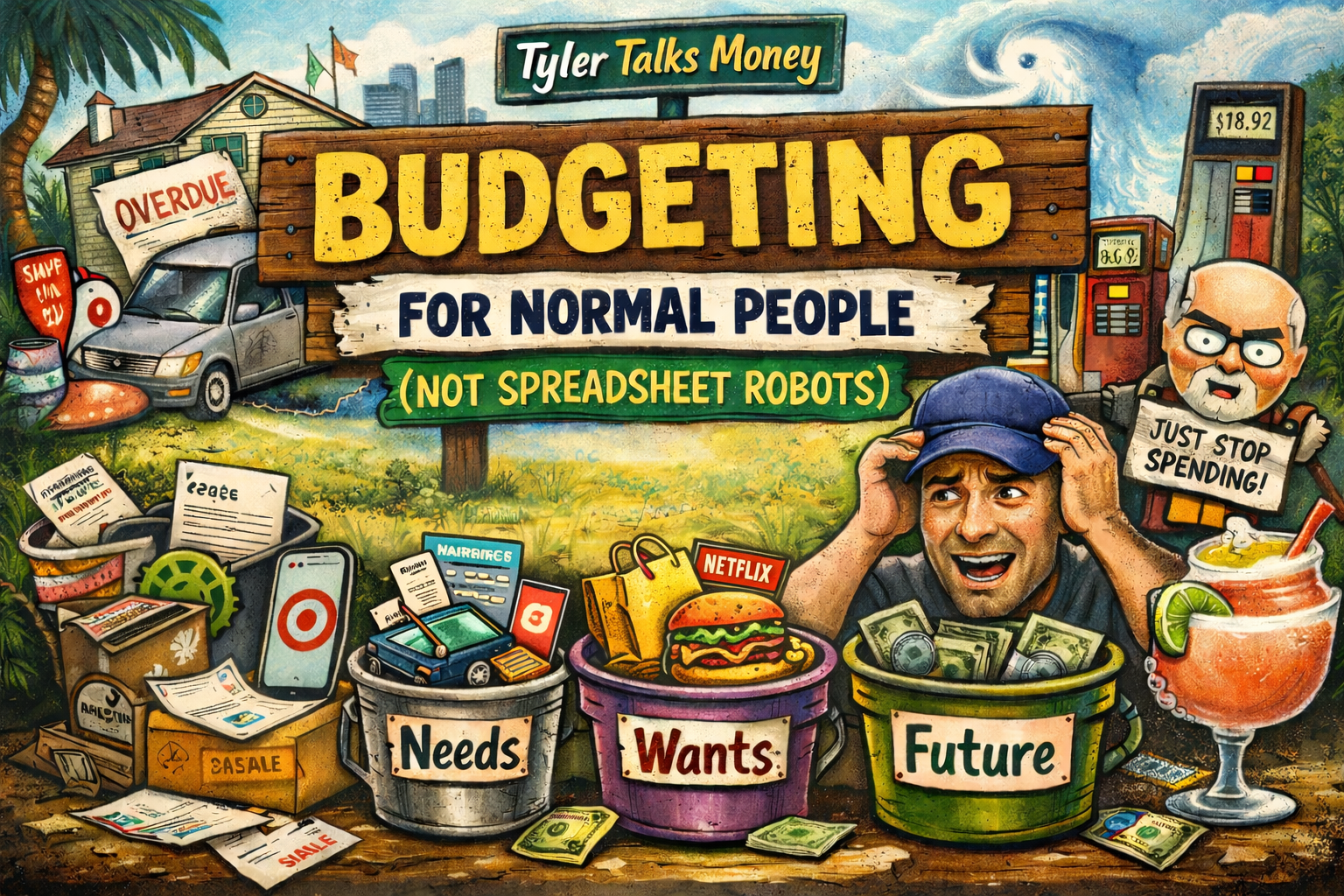

“JUST STOP SPENDING MONEY!”

Thanks Dave, truly groundbreaking. While we’re at it, I’ll also stop breathing, stop aging, and stop my kids from existing.

Down here in Louisiana, life isn’t “just stop spending.”

It’s crawfish boils, hurricanes, insurance that costs more than a small country’s GDP, and someone always selling raffle tickets for something.

Real people need real budgeting help.

Not shame.

Not yelling.

Not a guilt sermon from someone who hasn’t had a $7 travel ball concession stand emergency in 20 years.

Just something that works.

Why Most Budgets Crash and Burn

People don’t fail at budgeting because they’re dumb.

They fail because their budget looks like:

✨ Perfect fairy tale numbers

✨ Zero room for life

✨ Unrealistic expectations

💥 Explodes before the first paycheck clears

Then they go:

“Well that didn’t work. Guess I’ll just wing it.”

Budgeting shouldn’t feel like punishment.

It should feel like control… with your sanity intact.

Rule #1 — Your Budget Should Be Boring… and Built for Chaos

A budget is not a prison.

It’s not a diet.

It’s not a financial time-out.

It’s just a plan.

And plans need room for:

- surprise school fees

- birthday parties that materialize out of thin air

- nights when cooking feels illegal

- that one friend who always texts: “Let’s do dinner!”

Instead of designing a “perfect” budget Dave Ramsey would frame and hang on his wall, build a realistic one you’ll actually follow.

Rule #2 — Fix the Big 3 Before You Nitpick Lattes

Please stop stressing over $4 coffees while your house and car payments are tag-teaming your wallet like WWE wrestlers.

Start here:

1️⃣ Housing

Mortgage or rent.

Ideally under 30–35% of take-home pay.

If your payment feels like an abusive roommate you can’t evict… that’s why life feels tight.

2️⃣ Transportation

Cars are sneaky little money vampires.

Payments.

Insurance.

Gas.

Repairs. Every Louisiana pothole deciding to ruin your alignment.

If your car note feels like a second mortgage, congratulations — you bought a very pretty financial burden with wheels.

3️⃣ Food

The silent assassin of budgets.

Groceries + eating out + “Oops, we didn’t cook again.”

If you eat out a lot, do something wild:

Tell the truth and budget for it.

You’re not magically transforming into a gourmet chef next month.

Rule #3 — Use Buckets, Not 97 Tiny Categories

If your budget requires color coding, pivot tables, six sub-tabs, and a prayer… you’re not going to use it.

Normal people do better with simple buckets:

✔️ Needs

✔️ Wants

✔️ Future

That’s it. You are not the Department of Defense Finance Division.

If you want training wheels:

- 50–60% Needs

- 20–30% Wants

- 10–20% Future

Not perfect.

Not robotic.

But sustainable.

Rule #4 — Automate Because Willpower is a Myth

Let’s be honest: you are not going to remember to save every month.

Not because you’re irresponsible.

Because you’re busy and human.

Automate:

- savings

- retirement

- bills

Good decisions should happen automatically — not only after a motivational speech or a Ramsey podcast rant.

Rule #5 — If Your Budget Has No Fun, It Will Die

Humans do not thrive under misery budgets.

If your plan is:

❌ No fun

❌ No eating out

❌ No hobbies

❌ No joy

You will eventually launch your budget into orbit.

Build in:

- date nights

- hobbies

- vacations

- the occasional “I deserve this” purchase

Money is meant to be managed… not feared.

Rule #6 — Stop Chasing Perfection

Some months are ugly.

Some are expensive.

Some are just chaos.

That’s life.

The win is not perfection.

The win is progress.

Ask:

➡️ Do I know where my money went?

➡️ Did I spend intentionally?

➡️ Am I improving compared to last month?

If yes? You’re winning.

A Simple, Non-Stressful Budget You Can Actually Use

Copy it. Adjust it. Live your life.

🏠 Needs (55%)

Housing

Utilities

Groceries

Insurance

Car expenses

Debt payments

🎉 Wants (25%)

Eating out

Subscriptions

Amazon adventures

Entertainment

Kid chaos fund

🚀 Future (20%)

Emergency fund

Retirement

Investing

Extra debt payoff

Boom. Done. No yelling. No guilt. No financial cult energy required.

Final Thought

You don’t need to be perfect.

You don’t need to be a spreadsheet robot. Even though I think it’s fun, but I am of a select few.

You don’t need to swear off joy to be “good with money.”

You just need a plan that works in real life.

You’re not behind.

You’re just starting now.

And that’s exactly where progress begins.

Disclosure:

This content is intended solely for general financial education and discussion. It does not constitute advice, recommendations, or solicitation of any kind. The author is not providing services as a financial advisor, investment advisor, tax advisor, or legal advisor. All views expressed are personal and do not represent the views, policies, or positions of the author’s employer or any affiliated institution. No compensation has been received for this content. Any financial decisions should be made in consultation with appropriately licensed professionals.